What 3 Years of low-income sub-specialty training does to your savings rate?

The Cash Cost of Three More Years of Training

There is an opportunity cost of sub-specialty training. Not just in blood, sweat and tears of fellowship, but also salary.

Have you thought about what delaying an attending salary for 3 more years will cost you over time? Not just in opportunity cost, but in actual dollars and cents?

Let’s look a highly fictionalized scenario and see what the Cash Cost is of not being a hospitalist.

History of Present Illness

Assume we have a 30-year-old who either becomes a hospitalist or does a three-year fellowship. The hospitalist salary is $300k a year. If you chose fellowship, you will get $80k a year and then wind up making $400k a year as a sub-specialist.

To keep things simple, both have a 401k which they contribute 6% with a 6% match. Any extra money goes in a taxable brokerage account. Both accounts are invested in a Vanguard 2050 Target Date fund.

Assume inflation is 2%, and let’s start out with expenses of $64k a year which will go up with inflation.

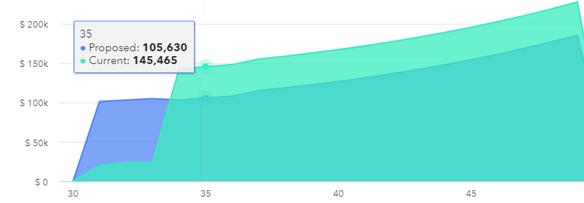

How does net worth change over time?

Net Worth over Time

Figure 1 (Net Worth over Time)

You can see in figure 1, we have the net worth over time from both plans. In dark blue, you are a hospitalist earning money right out of the gate. In Green, you do a fellowship and delay the higher attending salary for 3 years.

You can see both start rather slowly, but as savings rate is high with the attending salary, you start to build momentum.

It is not until you are 47, however, 17 years after you finish med school, that the deferred higher salary takes over. And in fact, after a full 20 years, the sub-specialist only has $240k more than the hospitalist.

Of course, both of these plans assume minimal life style creep. A high savings rate is maintained thorough out as expenses are only increasing by 2% a year.

Let’s look at taxes.

Taxes Owed

Taxes are a big deal here. As you earn more money, the last dollar you earn is exposed to the highest marginal tax bracket. In 2020, any income above ~$207k puts you in the 35% tax bracket. So, all of the money the sub-specialist makes hits the 35% tax bracket.

Both get to fill the lower brackets with income, which means the effective (or average) tax rate is lower for the hospitalist. In this example, the federal effective tax rate is 24% vs 27%. Not a huge difference, but let’s see what that looks like over time.

Figure 2 (Yearly Federal Income Taxes)

Above in figure 2, you can see the yearly income taxes due. As a fellow (green), you pay less in taxes, but that jumps up above the hospitalist (blue) when you make your sub-specialty income.

If we look out at age 35 when both are earning attending income, you can see the sub-specialist is paying about $40k more in taxes on the extra 100k in earnings. In fact, over 20 years, the sub-specialist pays $415k more in taxes. That averages out to about $21k a year more in taxes. Take that, sub-specialist.

Let’s get really wonky now and look at some cash flows. If you want, skip this section and join me again when we discuss account totals over time.

Cash Flows over 20 Years

Sub-Specialist

Figure 3 (Cash flows for the Sub-Specialist)

You can see the income for the first 3 years (I used 1% income inflation) for the fellow, and then the sub-specialist starting in 2023. Expenses go up over time by 2%, and you can see the tax payments each year. Note that there is a negative net flow during the fellowship, but net flows are quite fine while a practicing sub-specialist.

Also note I cut out some years to make the graph more digestible. Maybe this is a GI specialist. (Nope, income is not high enough…)

Hospitalist

Figure 4 (Cash flows for the Hospitalist)

Above, you can see the income starts higher for the Hospitalist from year one. Expenses are the same in both, but taxes and savings are different. Planned savings include the 401k, and everything left over gets invested in the brokerage account.

How do these cash flows affect the bottom line?

Account Totals Over Time

Ok, those less wonky should be back now to look at the account totals over time.

Figure 5 (Comparison of the Account Totals over time)

On the left we have the sub-specialist, and on the right is the hospitalist.

Note that the sub-specialist has no extra money to fund the taxable brokerage account and the 401k stops getting funded when he or she starts living off of credit cards in fellowship.

Compare that to the hospitalist on the right who immediately starts funding both.

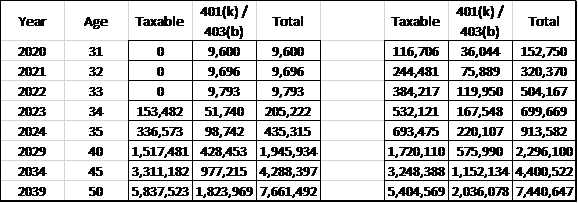

At the end of 20 years, you have $7.6M vs $7.4M, but the 401k never catches up given the late start.

Summary: The Cash Cost of Three More Years of Training

There is not only pain and suffering with fellowship, there is also a loss of income for several years.

In the example we have above, it takes 17 years to overcome the 3-year delay in earning. At the end of 20 years, there is not much difference due to the higher taxes paid on the higher salary.

Of course, in this example, we have someone who has a massive savings rate and minimal life style creep. Also, no student debt or mortgage is taken into account. There are many limitations baked into this example, but it is interesting to see how long it takes to catch up when you sign up for a higher, yet deferred, salary.

David Graham, MD is a practicing ID physician and Advice-Only Retirement Planner. He blogs at FiPhysician.com

You can read about Personal Finance For Hospitalists here.

![]()

Thanks for the guest post… looks good! Next, I will model an ID doc who takes a pay cut after three more years of training…